What is the best way to invest a lump-sum? Investors sometimes face this question – for example when they sell their business, when they inherit a significant sum of money, or perhaps when they win a lottery. In either case, they are dealing with a lot of liquidity that needs to be put to work.

Let’s assume our investor has USD12 million that they wish to invest for the long term. To keep things simple without a loss of generality, we will assume that the investor wants to allocate the entire sum to the global stock market.

There are many ways in which this can be done, but they can be classified in three main categories:

- simply investing everything immediately,

- dollar-cost-averaging, and

- waiting for a good entry point before investing.

In our example, dollar-cost-averaging would be done by splitting the 12 million into equally-sized tranches and deploying them over a period of 12 months.

On the other hand, those waiting for a good entry point will typically wait for the markets to correct by, say, 10 per cent before investing. To remove the risk of waiting for too long, they will invest the entire sum at whatever the price, if the dip does not occur over a certain period, say 12 months.

At this point, it is important to observe that, at the end of the 12-month period, the portfolio is fully invested in all three scenarios. Therefore, when comparing the effectiveness of these three approaches, we only need to compare the difference in performance over the first twelve months.

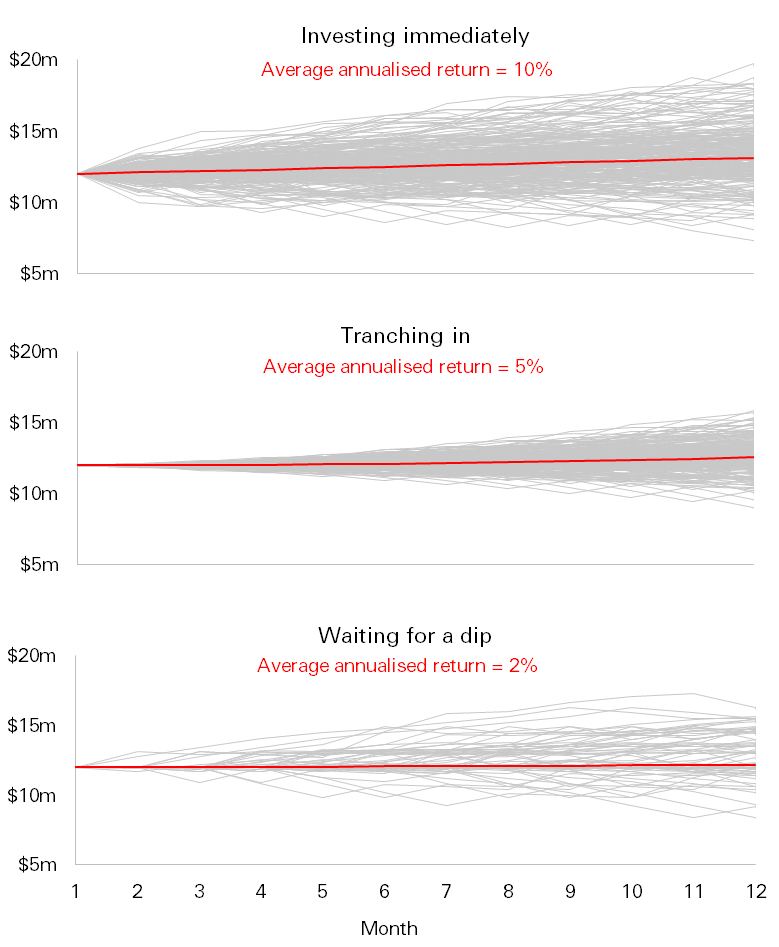

In our first chart, we can see the overall growth of USD12 million under all historical 12-month periods, starting from December 1969. In total, that is almost 600 different scenarios. Across all these 12-month periods, the average total return would have been around 10 per cent, or USD1.2 million for a USD12 million investment. Of course, due to market volatility, the range of outcomes could be anywhere between +USD7.8 million and -USD4.7 million.

Knowing that market returns have been positive historically, it should logically follow that any strategy that delays investment (such as tranching-in or waiting for a dip) should be expected to underperform in this backtest. Specifically, tranching-in delivers an average return of 5 per cent (compared to 10 per cent for immediate investing). This should not be surprising, as in this scenario, on average only half of the sum is invested during the tranching period.

The third chart shows that waiting for a dip would have generated an average return below 2 per cent. This is mainly because when you wait for the dip, you can keep waiting for a long time.

So, how do these three strategies compare? If our investor decides to wait for a dip instead of investing immediately, they should be expecting to be by around USD1 million less wealthy in 12 months. Of course, from that point onwards, this difference will continue to compound over time.

Tranching in versus investing immediately means that we are foregoing around half a million, simply by being only partially invested in the first year. Tranching in therefore is not as disadvantageous as waiting for a dip.

The conclusion should be intuitive. If investors are expecting the markets to rise, both logically and statistically (when we look at the data), investing immediately has the greatest expected return. Tranching in is the second best, and waiting for a dip is the worst option, from the expected return perspective.

That being said, anyone can imagine a horror scenario of investing at the worst possible time, just prior to a substantial market crash. While these are rare and unlikely events, due to their severity it is not difficult to understand the fear of deploying a large sum immediately. But, those who still wish to gradually deploy their money need to be aware of three main lessons:

- There is an expected cost to delaying investment, which is equal to the expected return of your strategy.

- This cost can be controlled by reducing the period over which they tranche in or wait for a dip. Phasing in over 3 months is generally less costly compared to phasing in over 3 years.

- There will always be a risk of an immediate selloff once the lump-sum is fully deployed, whether that’s done immediately or over a certain period of time. Therefore, this risk cannot be eliminated - it can only be delayed to a different date.